The future of money- Digital Cash/ Cash

Trade has always been the backbone of our civilisation and humans have always been looking for easier and more efficient methods for trading value.

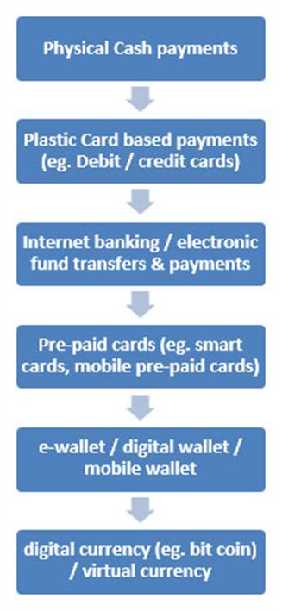

We started with barter, then came copper coins, gold and so on. Paper money was introduced to lessen the burden of carrying and exchanging thousands of copper coins and for the need of credit. Paper cash is popular amongst people as it is easy to carry, they can make payments with the received cash.

One of its major drawback is it can be stolen or lost and it is not convenient or safe to carry large sums of cash. Therefore we saw the introduction of plastic cards, electronic fund transfers, etc. And the next step in the automation of money is Digital Cash.

In a way, we have come full circle. We started with a cashless society and now we are heading towards the same again!

A system that allows a person to pay for goods or services by transmitting a number from one computer to another. One of the key features of digital cash is that, like real cash, it is anonymous and reusable.

- Advantages of using Digital Cash

- Saves time

- Reduce risk of theft

- Track and control expenses

- Enjoy greater privacy

- User-friendly

- Convenient (anytime, anywhere)

- Reduce black money and illegal activities

| Payment Options | Plastic Money | E-Wallet | USSD | Net/Mobile Banking | AEPS |

|---|---|---|---|---|---|

| (Credit card, Debit card) | (Mobile wallet) | (NEFT, RTGS, IMPS, UPI) | |||

| Issued By | Your bank | Companies like PayTM, Freecharge, etc. | Your bank | Your bank | Your bank |

| Use | Online payments- Card should be linked to your mobile number | Register for the services | Mobile number should be registered with the bank | Mobile number should be registered with the bank | Aadhar number should be linked to the bank account |

| Information required | PIN/ CVV Number, expiry date and registered mobile number | Login ID and password | MPIN/ IFSC/ Aadhar account number | Login ID and password, transaction password | Bank account number and Aadhar number |

| Transaction limit | Depends on bank and card | ₹ 20000 per month | ₹ 5000 per transaction | ₹ 10 lakh per transaction | Variable. Defined by the bank. |

| Advantage | Can be used online as well as at PoS | Best for small value transactions. Instant transfers | Accessed without internet or smartphone | Best for high value transactions. Instant transfers (IMPS or UPI) | Transact without card, phone or any paper |

Pause to ponder: Which of these did you consider during your last purchase?

- Caution: There is one form of comparison you must avoid or it will steal your joy. Unfortunately this is also the most common form of comparison. It is comparing what you have with what your friends may have.

- With the increase in digital transactions, cost of cash will reduce and this is expected to help us save ₹ 4.7 trillion between the years 2015 and 2025.

- • Word of caution: Internet security experts warn caution as India takes the cashless route, because this can be a big opportunity for cyber criminals to attack. This also presents an opportunity for growth in professions in areas like Cyber Security.

Cryptocurrency : A cryptocurrency is a digital or virtual currency that uses cryptography for security. It is created and held electronically. It is not issued by any government or central agency. No one controls it. It isn’t printed, like dollars or rupees. E.g. Bitcoins.

Fintech : Financial Technology, nowadays better known under the term 'fintech', describes a business that aims at providing financial services by making use of software and modern technology.

Of all the countries, Sweden is the closest to becoming a cash-free society. In Sweden, only 3% of all financial (money) transactions are in cash in comparison to 95% in India.

The use of credit cards originated in the United States during the 1920s, when individual firms, such as oil companies and hotel chains, began issuing them to customers for purchases made at company outlets.

1,000 and higher denomination notes were first demonetised in January 1946 and again in 1978. The highest denomination note ever printed by the Reserve Bank of India was the ₹ 10,000 note in 1938 and again in 1954.

Managing currency notes poses some specific problems. A farm in Delaware, US, mulches more than four tons of U.S. cash into compost every day. In previous eras, worn out bills were pierced or burned.

Like the serial numbers on real currency notes, the digital cash numbers are unique. Each one is issued by a bank and represents a specified sum of real money.

We shared some of the precautions to be taken in this digital age in the chapter ‘Better Safe Than Sorry’. Here are few guidelines specific to digital money transactions.

Online transactions

Avoid saving card data online

Pay online using OTPs

Before entering details on anywebsite, ensure it is a secure link. Web address should begin with 'https'

Avoid using personal data such as birth dates/names for passwords

Avoid using card-on-delivery option with new online retailers. It is safer to use digital wallets for paymentondelivery.

Mobile security

Use password manager applications (apps) that generate random passwords

Do not use the same password for digital wallets and net banking

Log out of digital wallets once a transaction is completed

Avoid installing third-party apps on your phone that pop up during ads

Activate mobile tracking to wipe out data remotely in case of device theft

Tab9

Tab10

- Next time you are out shopping, request an adult to let you make the payment digitally.

- You can try out:

- The POS machine at shops

- Pay online using credit/debit cards

- Pay using PayTM, Freecharge etc.

- Or any of the digital payment methods given in this section.